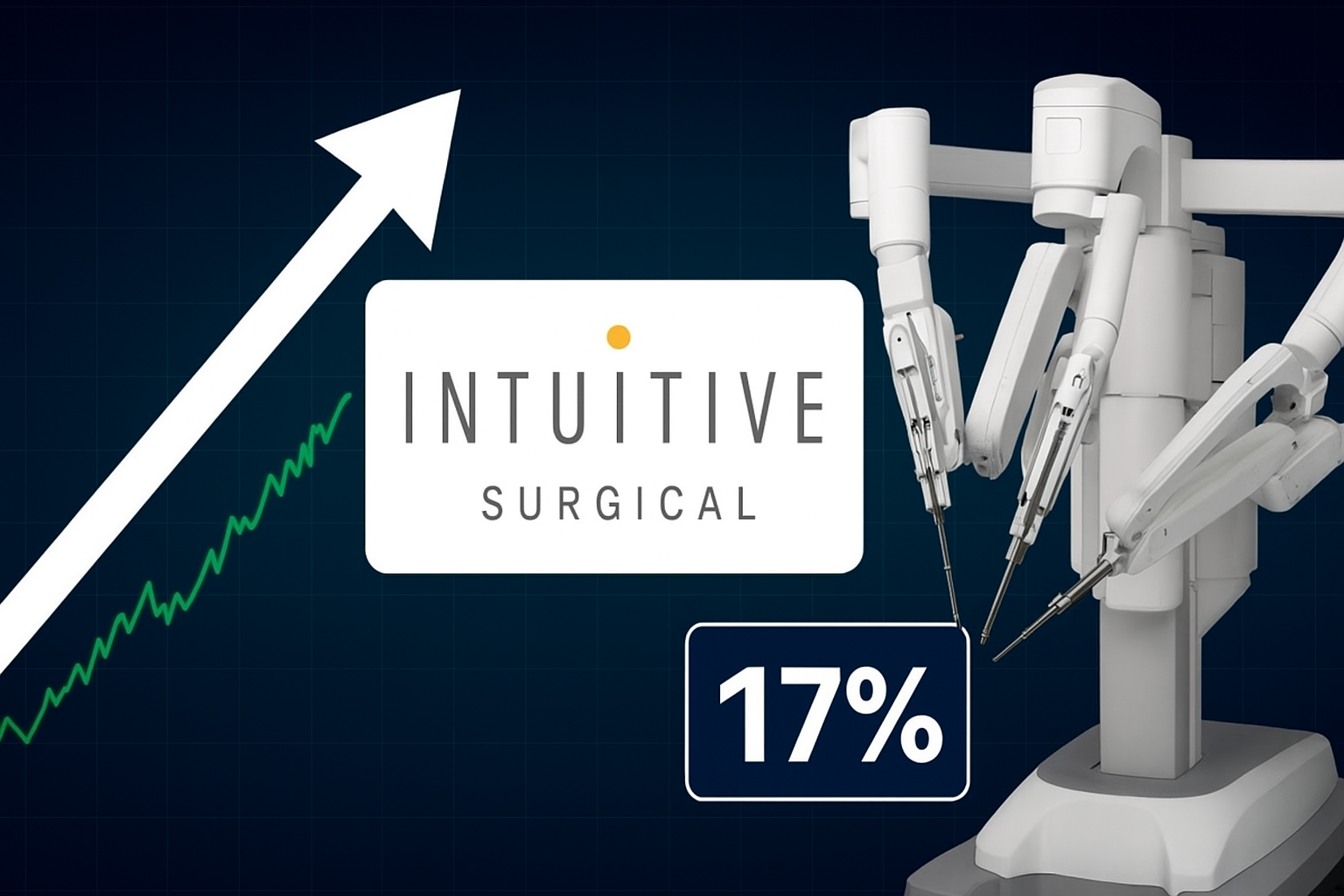

Shares of Intuitive Surgical jumped more than 17% in premarket trading on Wednesday after the robotic surgery pioneer reported stronger-than-expected third-quarter earnings, fuelled by the rising adoption of its flagship da Vinci system and expanding global demand for robotic-assisted procedures.

The California-based company posted adjusted earnings of $2.40 per share, surpassing the $1.99 consensus estimate among analysts polled by FactSet.

Revenue rose to $2.51 billion, beating expectations of $2.41 billion.

Intuitive placed 427 da Vinci surgical systems in the quarter, compared with 379 in the same period last year.

Its global installed base climbed 13% to 10,763 systems.

The number of procedures performed using the da Vinci and Ion platforms grew 20% year-on-year, with particularly strong uptake of the Ion bronchoscopy platform, which is used for lung biopsy procedures.

Shares began rising after Tuesday’s earnings release and continued higher on Wednesday.

Futures tracking the S&P 500 index were flat, underscoring the strength of Intuitive’s rally relative to the broader market.

ISRG retains its medtech leadership, say analysts

Analysts at Mizuho said the strong uptake of the da Vinci 5 in the United States more than offset weakness in markets such as Japan, China, and the UK.

“The third-quarter print shows Intuitive Surgical can maintain its bellwether medtech growth status,” they said, calling the performance a reassurance for investors who had feared market saturation in the US.

Intuitive raised its forecast for full-year worldwide da Vinci procedure growth to a range of 17% to 17.5%, up from prior guidance of 15.5% to 17%.

Growth in 2024 was 17%, suggesting continued momentum in the minimally invasive surgery market.

While some competitors such as privately held Restore Robotics are attempting to disrupt the space by reselling refurbished da Vinci accessories at lower prices, analysts say Intuitive’s scale, brand recognition, and deep integration with hospital systems give it a durable competitive edge.

Commentary around potential impacts from US healthcare policy changes — including Medicaid cuts and Affordable Care Act premiums — remained neutral.

Analysts noted that Intuitive is focused on helping healthcare providers manage costs and capacity, offsetting potential capital spending headwinds.

ISRG valuation debate reignites after rally

Following the sharp share price jump, some investors questioned whether Intuitive Surgical’s stock has become overvalued.

According to Trefis, ISRG shares currently trade at roughly 71 times reported earnings for the trailing twelve months, slightly below the four-year average of 75 times.

Adjusted for expected growth, the valuation remains in line with historical norms.

“Overall, ISRG stock offers a unique opportunity: monopoly-like high margins at a discounted price,” Trefis said.

“The company’s core strength lies in its pricing power and sustained profitability, which generate consistent, predictable profits and cash flows. This stability significantly reduces risk and allows for continuous capital reinvestment—qualities the market tends to reward,” it added.

However, the research firm also cautioned that Intuitive’s premium valuation makes it sensitive to market downturns.

The stock has historically fallen more steeply than the S&P 500 during periods of market stress.

During the 2022 inflation shock, ISRG shares dropped 50% from their peak, compared with a 25% decline for the broader market.

Similarly, during the early stages of the COVID-19 pandemic, the stock fell over 40%, compared with a 34% decline for the S&P 500.

“These historical patterns suggest that ISRG’s premium valuation makes it particularly susceptible to broader market volatility and economic uncertainty,” Trefis added.

Long-term outlook: should you buy?

Despite valuation concerns, most analysts view Intuitive’s growth trajectory as sustainable, given the accelerating adoption of robotic surgery worldwide.

The company’s consistent record of beating expectations, raising guidance, and maintaining strong profit margins highlights the strength of its competitive moat.

With growing hospital adoption of the da Vinci 5 system and increased utilization of the Ion platform, Intuitive appears well-positioned to capitalize on the global shift toward precision, minimally invasive healthcare.

“While the stock’s premium valuation requires sustained execution, the combination of strong procedure growth, expanding market opportunity, and proven operational excellence suggests that ISRG remains an attractive long-term investment despite the recent surge,” said Trefis.

The post Intuitive Surgical shares soar after upbeat earnings: should you buy? appeared first on Invezz

{kind=link}